Fintech experts are here to help you: Does embedded finance seem like a logical next step for your product, but seems a bit hard to do? Or perhaps you’ve started to research it but ended up with information (and acronym) overload?

We are striving to make this easier for you and have guides to help, but we wanted to delve deeper into the challenges and benefits of embedded finance for your product. So, we asked top fintech experts to share their thoughts on the topic.

As Oana Ifrim, Lead Editor on Embedded Finance at The Paypers, explains, “The financial landscape is rapidly evolving, with financial services becoming an integral part of the customer journey. Furthermore, partnerships with embedded finance providers are making banking-like services accessible to businesses of all kinds, blurring the lines between traditional finance and other industries.”

Promising use cases for embedded finance

Who is embedded finance for? When you think about convenient, well-designed, and digital financial services, it’s likely the brands you recognise or apps you use are those from banks or fintechs.

For fintechs, financial features embedded in their applications might be understood as the basis of their offering. But this isn’t embedded finance. The idea of embedded finance is to take those financial features that have already been successfully re-imagined as digitally native experiences by the fintech challengers, and take the idea a few steps further.

Here’s the definition of embedded finance we have on our wall at Weavr:

| The placing of a financial product in a non-financial customer experience, journey, or platform, and with the user experience under the non-financial brand rather than that of the bank or other financial services provider. |

Oana Ifrim advises: “In this rapidly changing financial world, embracing embedded finance is not just a trend; it’s a strategic necessity for businesses seeking to thrive in the digital era.”

Or, the McKinsey & Co variation:

From our experience with pioneers like finway, Ben, and NUMARQE, we know that embedding financial features is transformative for software businesses. But to know how this applies to your own industry and product, it helps to step back and see what makes a successful use case.

We asked a circle of industry experts for thoughts on the use cases that make them excited about embedded finance.

To begin with, Sam Boboev, COO and Co-founder at Botcommerce, provides some key themes where greater digitalisation of financial services is already significantly improving customers’ lives:

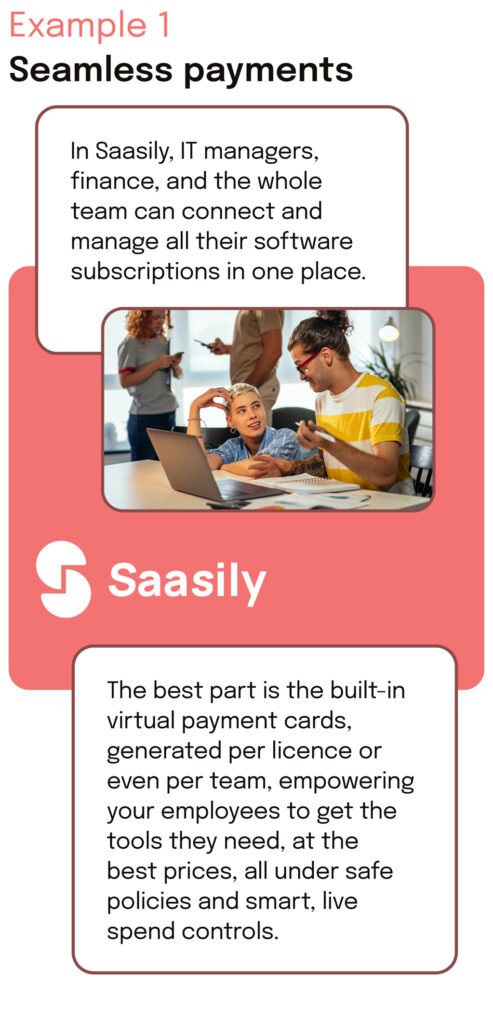

- Seamless payments

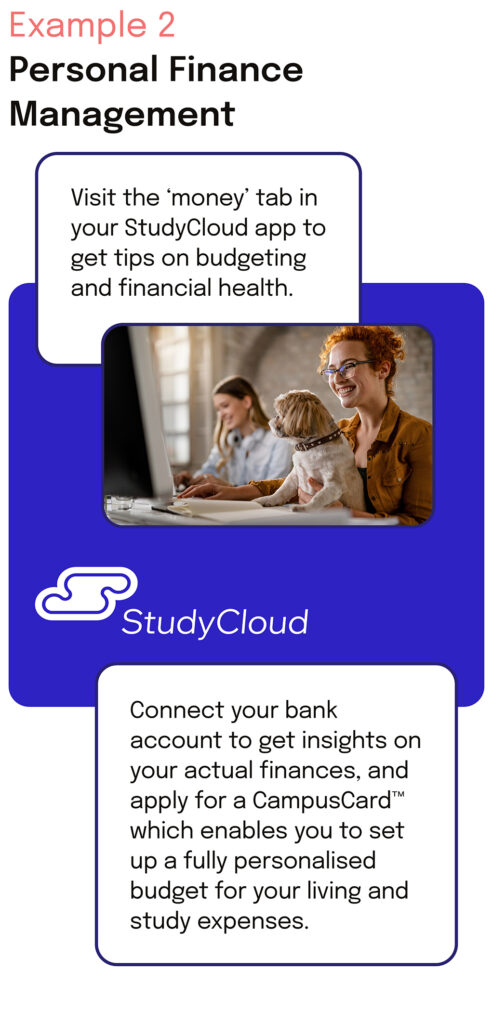

Integration of financial services within e-commerce platforms, mobile apps, or marketplaces can make payments more convenient and frictionless. For example, being able to complete purchases with a single click using embedded payment options. - Personal Finance Management

Embedded finance can offer users better tools for managing their personal finances and budgeting effectively. This could involve real-time transaction tracking, automated categorisation of expenses, personalised spending insights, and goal-setting features. - Investment and Wealth Management

Investors, increasingly ordinary retail customers, not only sophisticated or wealthy clients, can use well-designed digital services to easily access investment opportunities. Better integration of investment services within banking apps or other fintech solutions help people reduce complexity and manage their portfolios in one place. More joined-up data opens the possibility of more personalised recommendations based on individual objectives and risk profiles.

It’s possible to download apps that are specifically payment apps, or PFM apps, or investing apps, and so on. But embedded finance asks the question: what if these financial services were available closer to the point of need?

This means non-financial contexts, for example, consider these embedded finance use cases for illustrative purposes:

As Sam explains, “embedded finance has the potential to significantly enhance convenience, accessibility, and personalisation across various aspects of our daily lives by integrating financial services seamlessly into existing products and experiences”.

For example, “One favourite example already seen in the wild is ride-hailing companies integrating payment options directly within their apps so that users don’t have to switch between multiple applications for making payments after completing a ride. If we go deeper we can see that for example Uber is moving beyond simple payments for ride-hailing services and has an ambition of becoming a super application where payments and finance should play a crucial role.”

Another use case Sam mentions is insurance. Just like with other financial services, perhaps the winning innovations of tomorrow are not going to be designed in terms of a customer searching for an insurance broker or downloading an insurance app, but are going to be about identifying non-financial user journeys where insurance makes a lot of sense in each particular context. As Sam puts it, “Embedding insurance offerings into relevant products or services can simplify the process of purchasing policies tailored to specific needs such as travel insurance while booking flights or car insurance while buying a vehicle.”

And, as Panagiotis Kriaris, Commercial Director and Head of Business Development at Unzer, comments, the embedded finance opportunity is not just for consumer apps: “The embedded finance use cases most people have seen so far are in the B2C space, around convenient access to payments, financing, and insurance. But it is very likely that the next growth wave will come from the B2B side: sectors such as marketplaces, logistics, real estate, construction or energy.”

The growth is not just end user adoption but also a positive feedback loop for the embedders who succeed in delivering that improvement in the value of their application. Says Oana, “SaaS firms can readily establish synergy between their existing offerings and the evolving landscape of Embedded Finance. The integration of financial services not only enriches their product portfolio but also diversifies income sources, ultimately strengthening their competitive position.”

Shaul David – independent industry expert in BaaS, embedded finance and payments – expands on how embedded finance can generate a positive feedback loop: “In the case of embedded finance for digital marketplaces, the focus should be wide as value can be enhanced across the platform. Different embedded products solve different problems on both the supply and demand sides of the marketplace. That, in turn, creates higher levels of engagement for sellers and buyers. The ultimate result is a faster flywheel.”

If embedded finance is so great, why isn’t everyone doing it?

Embedded finance is quite widely adopted in certain application categories such as employee expense management and invoice financing. But in other areas like HR management, collaboration, or productivity, it’s still pretty rare to find financial features embedded into these apps, despite the fact that hot opportunities abound.

You might think that the simple reason is that embedded finance is too costly or difficult. But we think that before potential embedders even look into the “how” and “how much” of embedded finance, many have already dismissed it out of hand as something they don’t understand, something only relevant to fintechs or financial specialists. Sam comments “jargon and insider knowledge in the banking/payments industry can act as a barrier for non-financial innovators trying to understand and leverage the embedded finance opportunity”.

A big part of the problem is that the people building embedded finance and banking-as-a-service solutions are deep down in the details of payments, technology, and regulatory compliance.

Sam explains: “The concept of embedded finance involves integrating financial services into non-financial platforms or products, which requires an understanding of both finance and technology.”

But here’s what Shaul David said about a disconnect when experts try to explain: “Your solution is going to be API-based. But no one really needs to know what an API is. If a solution provider cannot spell out the value to the embedder in plain English, how will that person turn around and explain the business case internally? And more importantly, how will they drive value and conversation in their customer base?”

Sam adds: “Jargon such as APIs, Open Banking, KYC, AML, and other terms specific to the banking/payments industry can be confusing for individuals who are not familiar with these terms. It may take time for non-financial innovators to grasp the meaning and implications of such jargon, making it harder for them to fully comprehend how embedded finance works.”

We agree with Shaul and Sam – the answer to embedded finance, for a non-financial innovator, is not to force-feed yourself fintech jargon!

Sam explains it is not just the jargon that’s off-putting to newcomers, it’s the depth of knowledge required even if you understand the basic definitions: “Insider knowledge about regulations, compliance requirements, risk management practices, and market dynamics within the banking/payments sector is essential when considering opportunities in embedded finance. Non-financial innovators may lack this expertise initially and find it challenging to navigate through regulatory frameworks or identify potential risks associated with offering financial services.”

Is the answer just to get help from experts? Yes, but as Sam continues, that might not be easy either: “Building partnerships or collaborations with established financial institutions is often crucial in implementing successful embedded finance solutions. However, without prior connections or insights into how these institutions operate internally, non-financial innovators may face difficulties in establishing those relationships.”

As Sam concludes, would-be embedders could be forgiven for giving up: “Overall, while not insurmountable barriers, jargon and insider knowledge can pose initial challenges for non-financial innovators seeking to understand and capitalise on opportunities in the embedded finance space within the banking/payments industry.”

Can non-financial innovators integrate financial services?

We’ve mentioned that many innovative software companies might be ignoring embedded finance because of the off-putting jargon and apparently unavoidable complexity of assembling a viable solution.

But cost and complexity should not be insurmountable barriers. This actually was true for all but the biggest and most ambitious firms during what we might term the initial ‘trailblazing’ phase of embedded finance. But we’re beyond that by five or more years now: we’re in the early adoption phase for many proven embedded finance use cases.

As Panagiotis puts it: “There is a false understanding from some non-finance players that to employ embedded finance they need to have banking expertise, whereas the truth is that, if done right, it can be a plug-and-play experience.”

This does not mean that non-financial innovators should be reinventing the technology and model of the actual banking part – in fact they should not be considering building that part, but instead should focus on their options in the integration layer. As Shaul David explains, “The good thing about the industry being almost ten years on the embedded finance journey is that there are several viable operating models to choose from based on the level of internal banking expertise an embedder has. However, non-finance players must ensure the appropriate complementary expertise exist at their preferred partner and downstream from there.”

Some terms like “banking-as-a-service” and indeed well-known challenger banking brands may give the impression that, to do embedded finance, an innovator’s only choice is to compose a unique stack from a variety of technology components and disparate service providers. But for most would-be embedders, the key to making embedded finance strategy addressable is to avoid unnecessary costs and complexity in order to prioritise time-to-market.

Panagiotis concludes: “The great thing about embedded finance is that it can be flexible enough to be offered and consumed on a modular basis, which makes it a fit for organisations with different strategic, growth and buy or build priorities.”

Weavr’s CTO, Adrian Mizzi shared his views on the old-age strategy wrestle between ‘build vs buy’. Adding:

That question about build versus buy is crucial to understanding when a previously inaccessible innovation or technology becomes possible to adopt more widely, and that’s what is happening for embedded finance in many non-financial verticals.

Sam breaks down the strategy as follows:

“A firm that should consider a “buy” strategy on embedded finance is one with limited resources, expertise, or time to develop and maintain a custom-built solution.”

According to Sam, here are some factors that may indicate the suitability of a “buy” strategy:

- Limited technical capabilities

If your firm lacks in-house technology expertise or has limited development resources, purchasing an existing embedded finance solution can provide access to ready-made infrastructure and functionalities without requiring extensive technical know-how. - Time constraints

Building a bespoke embedded finance system from scratch can be time-consuming, involving various stages of development, testing, and deployment. If speed-to-market is crucial for your business objectives, buying an off-the-shelf solution may expedite the process. - Cost considerations

Developing custom solutions can be expensive due to hiring developers or outsourcing development work. If your firm is smaller e.g. a startup with budget limitations, buying into a pre-existing embedded finance platform is likely safer and lower cost than investing in building your own infrastructure. - Regulatory complexities

Embedded finance involves compliance with financial regulations such as anti-money laundering (AML), know your customer (KYC), data protection laws, etc. If your team are new to financial services, your organisation likely lacks the regulatory knowledge required and might find it easier to adopt an established solution that already addresses these regulatory requirements and offers access to solutions which are proven to be compliant. - Scalability needs

If scalability is critical for your growth plans but developing an in-house system would require significant investment in scaling up infrastructure and maintaining high-performance levels over time; adopting a buy strategy could allow you to leverage established tech that’s capable of accommodating growth without major disruptions or infrastructure costs holding you back.

Sam concludes that each would-be embedder should be willing to consider either approach – “buy” or “build bespoke”: “carefully evaluate your unique circumstances including budgetary constraints, resource availability/expertise, timelines/goals before making this strategic decision on how best to incorporate embedded finance into your product vision”.

That’s excellent advice and if you want to take the next step, head over and read Weavr’s Embedded Finance Buyer’s Guide where we will provide you with a set of questions to work through to pick the right strategy for your unique business, and hopefully get from embedded finance idea to embedded finance impact 10x faster.

Connect with leading embedded fintech experts

This article featured exclusive insights and advice from the following fintech experts – you can connect with each of them via the LinkedIn link in their profiles below:

Thank you so much Oana, Panagiotis, Shaul, and Sam – talk about an embedded finance dream team!

If you want to know more on the topic of ‘what is embedded finance?’ and what that means for your business, check out our ultimate embedded finance guide here.