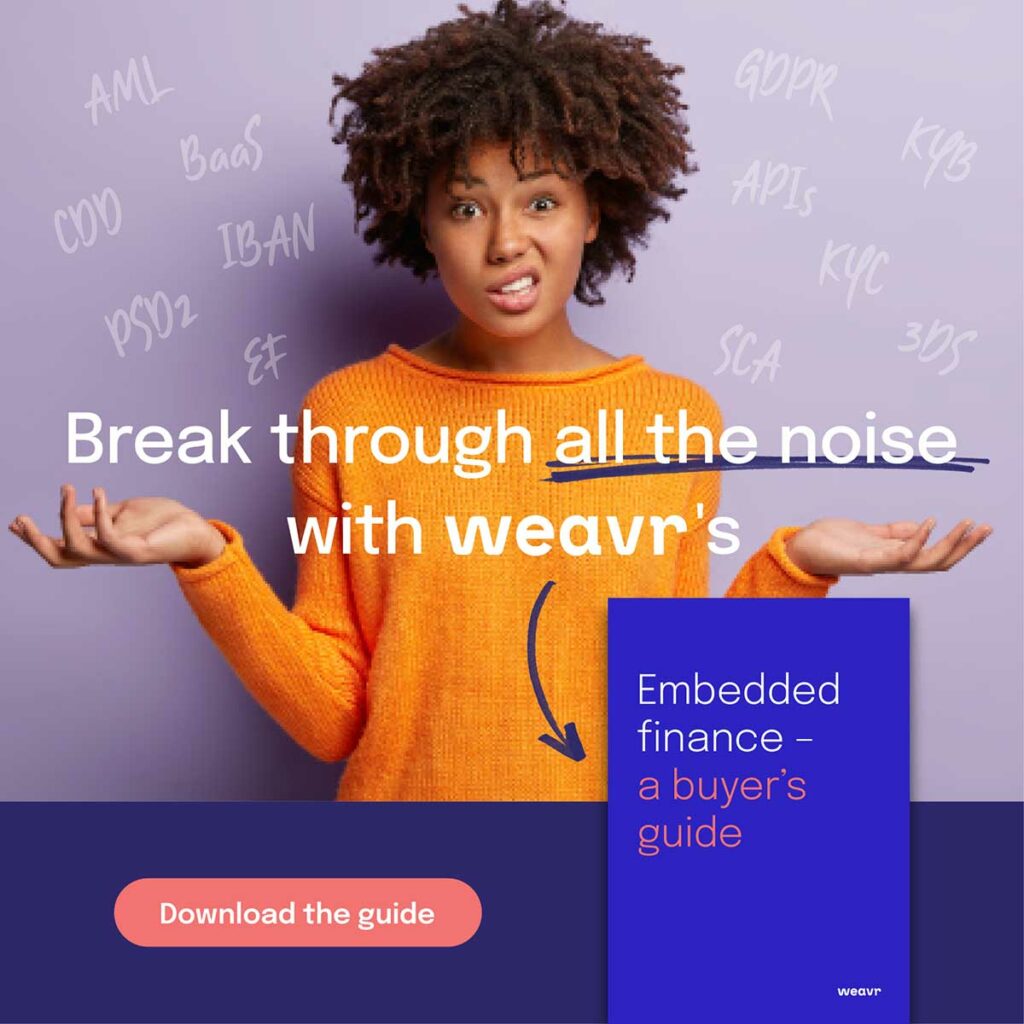

Like many industries, embedded finance is littered with acronyms and buzzwords. Even those of you who are well-versed in industry jargon sometimes have to Google the meaning of lesser-known ones. We’ve compiled this fintech finance glossary of terms to help.

No more getting lost down rabbit holes of research, no more asking “what is …”. We’re here to help you break through all that noise to glean a clearer understanding of how embedded finance can help your business and to provide you with clear definitions of many of the phrases used when discussing embedded finance.

Do you have any to add that you don’t currently see on the list? We welcome additions to the fintech glossary of terms and want it to be up-to-date to help demystify the industry jargon. You can send in your glossary suggestions via our Contact Us page here

Misc

3-D Secure (3DS)

3-D secure (3DS) is a security protocol used in online card transactions. 3DS adds an extra layer of authentication ensuring that, when a person makes a purchase, they are the legitimate cardholder. The process involves using a one-time password, biometric verification, or other similar methods. This helps reduce the risk of fraudulent transactions and ensures consumers’ and businesses’ peace of mind.

A

Access token

An access token is a digital key that allows access to specific resources or services online. It is commonly used for authentication and authorisation. When a user or application requests access to a protected resource, they present an access token as proof of their identity and entitlement to access that resource.

Account Information Service (AIS)

Account Information Service (AIS) is a financial service used by third-party providers to access a user’s financial information from multiple banks and institutions. AIS providers give an overview of things such as user’s financial data, budgeting, financial planning and much more.

Account Information Service Provider (AISP)

Regulated Account Information service provider (AISP) offers Account Information Service (AIS). They help users manage their finances by blending account information from various banks and financial institutions in one interface.

Account Servicing Payment Service Provider (ASPSP)

Account Servicing Payment Service Provider (ASPSP) is a financial institution that provides and maintains payment accounts for customers.

Account Verification

Account verification is the process of confirming the authenticity and accuracy of financial accounts. It involves checking ownership, balances, and account information. This is important for secure transactions and regulatory compliance.

Accounts Payable

Account Payable (AP) refers to the money a business owes to it’s creditors/suppliers for goods and services, Until it’s paid, it’s a liability on the company’s balance sheet.

Accounts Receivable

Money owed to a business by its customers for goods and service is known as Account Receivable (AR), It’s an asset on a company’s balance sheet.

Alternative lending

Alternative lending is a non-traditional method of providing loans or credit. This includes peer-to-peer lending platforms, online lenders, and crowdfunding. Alternative lending has more flexible terms compared to traditional banks, which has made it gain popularity.

Anti-Money Laundering Directive (AMLD)

Anti Money Laundering Directive (AMLD) is a European Union Directive intended to prevent money laundering and combat terrorism financing. It provides that obliged entities shall apply customer due diligence requirements when entering into a business relationship (i.e. identify and verify the identity of clients, monitor transactions and report suspicious transactions)

Anti-money laundering (AML)

Anti- Money Laundering Laws are intended to prevent criminals from disguising the origin of illegally obtained funds and make them look like legitimate income.

API (Application Programming Interface)

Application Programming Interface (API) is a set of rules that allows different software applications to communicate and interact with each other. It enables developers to access the functionality of other applications or services, making it easier to build software and integrate.

API Banking

Application Programming Interface used in the financial industry is known as API Banking. It allows banks and financial institutions to offer their services and make seamless integration for programmers. It increases the efficiency of financial transactions and services.

Apple Pay

Apple Pay is a digital wallet that allows users to store physical cards in their e-wallet, which they can use to make payments. It’s secure, convenient, widely used and accepted by merchants all around the world. Read our blog on “The benefits of Google Wallet and Apple Pay in the corporate world”

Asset Management

Asset Management involves professionally managing investments and assets for individuals, institutions, or entities. Asset managers make investment decisions to maximise returns while managing risk. This service is important for individuals and organisations seeking wealth growth.

Authentication factor

Authentication Factors are different ways a user can verify their identity, Some of the factors include something a user knows (password), something they have (mobile device) or something they are (fingerprint or facial recognition). Multi-factor authentication combines two or more of these factors, for maximum security.

Authorised Push Payment (APP) fraud

Authorised Push Payment (APP) happens when a victim gets tricked into authorising a fraudulent payment. The victim approves the payment, usually due to social engineering or deception. Unlike unauthorised transactions.

Automated clearinghouse (ACH)

An automated Clearinghouse (ACH) is a system that makes it possible to do electronic money transfers and payments between banks and financial institutions. ACH transactions are commonly used for direct deposits, payments, bills and other electronic transfers.

Automotive finance

Automotive finance is the financing option for purchasing vehicles. These include loans, leases and other finance products found in the automotive industry.

B

B2B Payments Ecosystem

The B2B Payments Ecosystem is the network of financial processes and transactions in business-to-business payments. It encloses payment methods, technologies and service providers that exchange funds between businesses.

BaaS marketplace

BaaS (Banking as a Service) marketplace means the ecosystems where banks and financial institutions offer their services and products with the use of API to third-party developers. It promotes innovation and gives access to banking services for startups and developers.

BACS

BACS (Bankers’ Automated Clearing Services) is a payment system in the UK for electronic payments, including direct debits and credits. It automates financial transactions.

Balance

A balance represents the financial status of an account, showing the difference between credits (deposits or income) and debits (withdrawals or expenses). There are two types of balance- actual and available. Actual balance is the total amount of money on a customer’s account including any pending transactions. Available balance is what is available for the customer to use out of this actual balance – typically this is the actual balance minus any pending transactions.

Bank account

A bank account is a financial account provided by a bank. It allows depositing, withdrawing, and managing funds securely.

Banking as a platform

Banking as a platform is when banks open up their infrastructure and services to third-party developers and businesses through APIs. This promotes innovation and allows for the development of new financial products and services.

Banking as a Service (BaaS)

Banking as a Service (BaaS) is when banks provide banking services, like payments, account management, and lending, to third-party providers through APIs. BaaS allows businesses to integrate financial services into their applications and platforms. Read our blog to discover “Banking as a Service vs embedded finance: what’s the difference?”

Banking charter

A banking charter is an official license or authorisation provided by regulators, giving an institution the go-ahead to be a bank and offer all those banking perks to customers.

Banking license

A banking license is a legal permit given by regulation authorities that gives an entity authority to operate as a bank and be able to offer banking services.

Basel III

Basel lll is a set of international banking regulations made by the Basel Committee on Banking Supervision. It’s in place to strengthen and stability in the banking sector by imposing stricter capital and liquidity requirements for banks.

Biometric

Biometrics uses special physical or behavioural traits like fingerprints, facial recognition, and voice recognition to confirm a person’s identity, adding a very strong layer of security to authentication.

Bitcoin

Bitcoin, a digital currency functioning on blockchain technology, Bitcoin enables direct peer-to-peer transactions, it eliminates the necessity for intermediaries like banks. serving both as a store of value and a digital exchange medium.

Blockchain

Blockchain is a distributed ledger technology, that records transactions securely across multiple computers with transparency. Beyond being the foundation for cryptocurrencies like Bitcoin, it also finds applications in areas such as supply chain management and voting systems.

Borrower

A borrower can be an individual, business, or entity that receives funds from a lender under the agreement to repay the borrowed amount, usually with interest, within a specified timeframe.

Buy now, pay later (BNPL)

Buy now pay later (BNPL) is a payment option that lets customers make purchases and delay payment until a later date, making it an increasingly popular alternative to traditional credit.

C

CAPTCHA

CAPTCHA (Completely Automated Public Turing test to tell Computers and Humans Apart) safeguards websites by recognising between human users and AI bots. Users prove their humanity by solving puzzles or entering numbers or characters.

Card Acquiring

Card acquiring is the process through which businesses or merchants accept card payments (debit or credit) from customers. The acquiring bank facilitates the transaction, depositing funds into the merchant’s account.

Card Issuing

Card issuing is the creation and distribution of debit and credit cards by financial institutions, it involves activities like card production, activation, and management.

Card Scheme

A card scheme refers to a network or association establishing the rules and standards for using payment cards. This includes cards such as Mastercard and Visa. It is the process by which cardholders, merchants and issuing and acquiring banks are connected to enable card-based transactions.

Cardholder

The cardholder is the individual or entity that holds and uses the payment card. This can refer to a debit card or a credit card and can be used to make purchases.

Cardholder present (CP) and cardholder not present (CNP)

Cardholder present (CP) and cardholder not present (CNP) refer to the different transaction modes that indicate whether a cardholder is physically present at the point of sale or not. CP transactions occur when the cardholder is present, while CNP transactions occur in remote or online purchases.

Central Bank Digital Currency (or CBDC)

The term Central Bank Digital Currency (or CBDC) refers to a digital form of a country’s national currency that is issued and regulated by its central bank. The currency sits alongside physical cash and traditional bank deposits and is used to enhance payment efficiency and financial inclusion.

Challenger Bank

A challenger bank refers to a smaller, innovative financial institution that is challenging traditional banks by offering an alternative modern, digital-first banking experience and services. They are often seen to be more focused on user-friendly customer-first interfaces and features.

Chargeback

A chargeback is a dispute resolution process that is initiated by a cardholder to start the process of reversing a credit card transaction. This occurs when a cardholder believes that a transaction could be fraudulent or unauthorised.

Chip and PIN

The technology referred to as Chip and PIN is a security technology that is used in modern payment cards. It is made up of a microchip that is embedded in the card which generates a unique code for each transaction. A user of the card must enter a personalised identification number (PIN) in order to authorise payments.

Client Money

The term ‘client money’ refers to funds that are held by a financial institution on behalf of an individual client or customer. These funds are separate from an institution’s own funds and are subject to specific regulatory requirements which protect the client’s interest.

Companies Register

A companies register is an official and public database or repository where information is stored about registered companies. This can include their legal status, ownership and financial data which is stored and made publically accessible.

Compliance

Compliance is used to refer to the adherence to laws, regulations and industry standards within a specific business or financial context. Compliance can involve implementing policies and procedures to ensure that an organisation and individuals within an organisation operate within legal as well as ethical boundaries.

Consumer Duty

Consumer duty is the regulatory initiative that is aimed at ensuring that financial service providers act in the best interest towards their customers. Consumer duty puts the emphasis on transparency, fair treatment and appropriate production recommendations to the end user.

Core Banking

The term core banking refers to a central infrastructure and software system that is used by a bank to manage core financial functions. These functions include deposits, loans and customer accounts. Core banking forms the backbone of all banking operations.

Corporate Spend Card

A corporate spend card is a payment card that is issued to employees of a company for all business-related expenses. A corporate spend card can help to manage and track company expenditures while providing employees with a convenient way to make purchases without using their own funds. To find out how embedded finance can help with corporate spend cards check out our guide to “how embedded finance can empower employees”

Counter financing of terrorism (CFT)

Counter financing of terrorism (CFT) refers to measures and strategies undertaken to prevent terrorist organisations from accessing funds to support their activities. Financial institutions and companies play a critical role in implementing CFT measures.

Creator economy

A creator economy encompasses individuals, often creators of content, influencers or artists who have monetised their skills, content or creations through digital platforms and technologies. It represents a shift in how individuals can earn income and build their careers. To find out how embedded finance can help the creator economy check out our plug-in for worker finance

Credit Card

A credit card is a form of payment card that allows a cardholder to make purchases on credit. The card works on the promise that the cardholder will repay the borrowed amount, often with interest added or at a later date. It offers a convenient and revolving line of credit to the cardholder.

Credit Score

A credit score is a numerical representation of an individual’s creditworthiness. This is based on their credit history and financial behaviour. A credit score is used to assess the risk to a lender when deciding whether to lend to a borrower.

“If you are Apple-like obsessed with your customer experience and brand, then the only choice is embedded finance that is truly seamless”

Alex Mifsud, CEO, Weavr

Cross-border payment

Cross-border payments are financial transactions that occur between an individual, business or financial institution who are based in different countries. These transactions can involve currency conversions and are often subject to international regulations.

Cryptocurrency

The term cryptocurrency refers to a digital or virtual form of currency that uses cryptography for security. Cryptocurrency operates on decentralised technology, typically this is the blockchain and allows for peer-to-peer transactions without the need for intermediaries or traditional financial institutions.

Cryptocurrency Exchange

A cryptocurrency exchange is a platform that facilitates the trading of cryptocurrencies. This allows users to buy, sell and exchange different forms of cryptocurrencies in a secure and regulated environment.

Cryptocurrency on/off ramp

Cryptocurrency on/off ramp refers to a service or platform that enables individual users to convert traditional currency (on-ramp) into cryptocurrencies or vice versa (off-ramp). Cryptocurrency on/off ramps serve as an entry and exit point between crypto and traditional financial systems.

Current Account

A current account is also referred to as a checking account and is a basic bank account that allows an individual or business to deposit, withdraw and use funds for everyday transactions.

Customer Acquisition Cost (CAC)

Customer Acquisition Cost (CAC) in fintech refers to the expenses of acquiring a new customer. It includes resources and financial outlays. It is an essential indicator in the fintech industry and is often used with the LTV metric to evaluate the value of acquiring a new customer.

Customer or Client Due Diligence (CDD)

Customer due diligence (CDD) is the process undertaken by financial institutions and other regulated businesses to verify a customer’s identity and assess any potential risks associated with such a customer. To undertake CDD a financial institution or other regulated business must gather information about customers, this information will include their identity, source of funds and financial activities. This is done to ensure compliance with anti-money laundering (AML) Combating of Financing Terrorism (CFT) regulations.

Customer Experience (CX)

Customer experience (CX) refers to the overall perception and satisfaction of customers when interacting with a brand, product or service. This can encompass all touchpoints and interactions, including but not limited to website visits, sales experience, and face-to-face interactions. The goal of customer experience is to create a positive, seamless and memorable experience which will lead to customer loyalty and an increase in returns and recommendations.

Customer Lifetime Value (LTV)

Customer Lifetime Value (LTV) is a key metric, representing the total expected value a customer brings to a financial technology company throughout their relationship. LTV provides insights into the long-term economic impact of acquiring and retaining customers, helping fintech businesses make strategic decisions and determine the overall profitability and sustainability of their customer relationships over time.

D

Data Aggregator

A data aggregator is an entity or service which collects, processes and consolidates data from multiple sources into one centralised repository. A data aggregator plays a crucial role in data analysis, reporting and providing valuable insights into a business and its customers.

Data Privacy

Data privacy is the protection of an individual’s information and data from unauthorised and unwanted access, use or disclosure. This is closely linked to and involves compliance with privacy regulations and the implementation of security measures to ensure the safeguarding of all sensitive data.

Debit Card

A debit card is a payment card that’s linked to a bank account. This debit card allows the account holder to make purchases and withdraw funds when needed. Debit cards use the account holder’s money, unlike credit cards.

Decentralised Finance (DeFi)

Decentralised finance (DeFi) is a blockchain-based financial ecosystem. It provides financial services without relying on intermediaries such as banks, exchanges, and brokerages by using decentralised networks and smart contracts.

Deposit

A Deposit is the act of putting money or assets into a bank account or financial institution for safekeeping, savings, or investment purposes. This can include cash, checks, or electronic transfers.

Deposit Account

A Deposit Account is a type of bank account that is used for keeping hold of deposited funds. Some examples include savings accounts and checking accounts, each with its own features tailored to the purpose.

Deposit Insurance

Deposit Insurance is a protection mechanism given by governments or regulatory authorities that ensures a certain level of coverage for depositors’ funds in a case of bank’s failure. It provides confidence in the banking system.

Digital Asset

A Digital Asset is a digital representation of a real-world asset. It includes cryptocurrencies, digital tokens, digital certificates, and more. Digital assets are usually very secure and transacted using technology known as blockchain.

Digital Banking

Digital banking is the digital technology and online platforms that are used by financial institutions. It provides a wide range of banking services to customers and enables customers to manage transactions, accounts, and access financial services from a web or mobile application.

Digital Wallet

A digital wallet is a software application that allows users to store, manage, and organise the different forms of digital currencies, this also includes cryptocurrencies and traditional fiat currencies. It helps increase convenience and security in online and mobile payments.

Direct Debit

Direct Debit is a payment method that allows businesses or service providers to withdraw funds directly from a customer’s bank account, to pay invoices. It’s a convenient and very automated way to make repeat payments.

Distributed Ledger Technology (DLT)

Distributed Ledger Technology (DLT) is a digital system used for recording and verifying transactions across multiple networked computers. It is the main foundation for blockchain technology and it is used for creating transparent, secure ledgers.

Dynamic Linking

Dynamic linking is a feature in payment authentication processes, this is where the transaction’s details are linked to the user’s identity or device. It increases security by making sure the transaction data cannot be reused for any fraudulent purposes.

E

E-money

E-money (electronic money) is the digital version of fiat currency stored electronically. It is used for online transactions, mobile payments, and digital wallets. E-money is usually issued by financial institutions or electronic money institutions.

E-money institution

An E-money institution (EMI) is a financial entity licensed to manage electronic money. It is very important in facilitating digital payments and electronic fund transfers.

Electronic Identity Verification (eIDV)

Electronic Identity Verification (eIDV) is the process that uses digital documents and biometrics to verify a person’s identity. It’s usually used for security and compliance, such as Know Your Customer (KYC) checks.

Embedded Finance

For a more in-depth review of “what is embedded finance” please check out our “Ultimate guide to embedded finance”

Embedded payments

Embedded payments are financial transactions seamlessly woven into non-financial applications. Examples include purchases in-app, payments for ride-sharing, and online checkout processes.

Embedder

In fintech, an embedder (also see innovator) is an individual or entity engaging with a financial technology service, utilising products such as banking, investment, or payment solutions. The term encompasses those who actively participate in and benefit from the offerings provided by fintech platforms, shaping the user base and driving the industry’s growth and innovation.

Employee benefits

Employee benefits are provided by employers to employees as compensation outside of their monetary compensation. Example benefits include health insurance, pension contributions, paid time off, and other rewards designed to attract and retain talent. To find out how embedded finance can help with employee benefits check out our guide to how embedded finance can help empower employees

Endpoint

An endpoint is a device or node in a network, e.g. a computer, mobile phone, or internet-connected device, where data is sent or received. Endpoint security is of key importance in protecting against cyber threats.

Enhanced Due Diligence (EDD)

Enhanced Due Diligence (EDD) is a risk management process characterised by greater scrutiny when assessing the customers’ backgrounds, particularly in the context of anti-money laundering (AML) and Know-your-customer (KYC) regulations. In most cases, it involves collecting more detailed information and conducting additional checks to mitigate potential risks. In general, the EDD shall be carried out on high-risk customers.

Environmental, social, and corporate governance (ESG)

Environmental, social, and corporate governance or ESG is a set of criteria employed by organisations and investors to measure a company’s impact on the environment, social responsibility, and corporate governance practices. It is a framework for assessing a company’s sustainability and ethical practices.

European Banking Authority (EBA)

A regulatory agency of the European Union (EU), The European Banking Authority (EBA) is responsible for ensuring the integrity and stability of the European banking sector. With the ultimate objective of maintaining financial stability, it develops regulatory standards and performs stress tests.

European Central Bank (ECB)

As the central bank for the euro currency, The European Central Bank (ECB) is responsible for Eurozone monetary policy. It manages the euro currency, determines interest rates, and tracks the financial stability of the Eurozone.

European Economic Area (EEA)

The European Economic Area (EEA) is an extension of the EU’s single market that also incorporates non-EU countries in Europe such as Iceland, Liechtenstein and Norway. The agreement provides for the free movement of goods, services, people, and capital in EU member states and EEA countries.

Expenses

Expenses are costs incurred by individuals, businesses, or organisations in the pursuit of business or personnel goals. They can include costs such as wages, office rentals, utilities, and more. Read our guide on how embedded finance helps with employee expenses.

F

The Faster Payments Service (FPS)

The Faster Payments Service (FPS) is a banking initiative in the UK that provides real-time electronic money transfers and payments between banks and financial institutions. The result is quicker and more efficient transactions.

Federal Deposit Insurance Corporation (FDIC)

A U.S. government agency, The Federal Deposit Insurance Corporation (FDIC) provides insurance on deposits to banks and savings associations. It safeguards the funds of the depositor in the context of bank failures.

Fiat Currency

Fiat currency is a government-issued currency that is declared to be legal tender for transactions within a specific jurisdiction. Fiat currency relies on the trust and authority of the government and, as such, is not backed by a physical commodity like gold.

The Financial Action Task Force (FATF)

The Financial Action Task Force (FATF) is an intergovernmental organisation that defines global standards for countering money laundering, blocking terrorist financing, and preventing other financial crimes. It produces guidelines and recommendations for measures relating to AML/CFT.

The Financial Conduct Authority (FCA)

The Financial Conduct Authority (FCA) is the UK regulatory body responsible for regulating and overseeing the financial services industry, ensuring the protection of consumers, and fomenting competition in the financial sector.

Financial crime

Financial crime covers a range of illegal actions within the financial sector, such as fraud, money laundering, corruption, bribery, and financing terrorists. It represents a risk to financial institutions and the economy at large.

Financial Inclusion

Financial inclusion is the objective to ensure access to financial services – for example, banking, insurance, and credit – to both individuals and communities who are typically underserved or excluded from the formal financial system.

Financial Institution

A financial institution is a regulated entity that offers financial services to individuals, companies, or governments. Examples include banks, credit unions, and investment firms.

Financial Services Compensation Scheme (FSCS)

The Financial Services Compensation Scheme (FSCS) is a programme backed by the UK government. It protects consumers by compensating them when a financial institution cannot meet its obligations and is thus insolvent.

Fintech

Fintech is a term used to describe financial technology. This often refers to the innovative use of technology to provide consumers and businesses with financial services. This can include banking, payments, investments as well as insurance services. Modern Fintech companies use digital platforms, data analytics and automation to offer an efficient and user-friendly solution to their clients.

First-Party Fraud

The term First-party fraud refers to when an individual or entity engages in fraudulent activities using their own identity or accounts. Examples of First-party fraud are activities such as loan fraud, credit card fraud, or identity theft for personal gain.

Fraud

Fraud is defined as a deliberate and deceptive act carried out with the intent to gain an unfair or unlawful advantage. Fraud is mostly associated with deceit, misrepresentation or concealment of information in order to gain a financial advantage and personal gain. The term fraud encompasses a wide range of dishonest activities, including but not limited to creating false statements, forgery, identity theft, embezzlement as well as many other forms of deceitful practices all aimed at defrauding individuals, organisations or the general public.

G

General Data Protection Regulation (GDPR)

The General Data Protection Regulation (GDPR) is a comprehensive data protection and privacy regulation in the European Union. The regulation establishes and enforces rules for the collection, processing, and storage of personal data, ensuring individuals’ privacy rights are respected.

Gig Economy

The term gig economy is used to refer to a labour market made up of short-term, freelance, or contract work arrangements rather than people characterised as being in traditional full-time employment. For more information about how embedded finance works within the gig economy industry click here

Google Wallet / Google Pay

Google Pay (formerly Google Wallet) is a digital payment service developed by Google. They allow users to store payment information securely; usually on a mobile device and make online and in-store payments without the need for a physical card. Click here for information about how Weavr uses Google Wallets for embedded finance debit cards

H

High-Net-Worth Individual (HNWI)

A high-net-worth individual (HNWI) is an individual defined as having substantial wealth and financial assets. Typically a HNWI will have a net worth well above the average for the country they reside in and often require specialised financial services and wealth management.

I

IBAN

The International Bank Account Number (IBAN) is a standardised international numbering system used to identify bank accounts worldwide. It helps facilitate cross-border transactions and ensures accuracy in international money transfers.

Identity and Verification (ID&V)

Identity and verification (ID&V) is a process of confirming a person’s identity, this is usually done through a review of documents, biometrics, or digital means. ID&V is used to prevent identity theft and fraud in industries such as banking and online services.

Impersonation Scam

The term impersonation scam is when an individual pretends to be someone else, this is often done to a trusted entity or authority in order to deceive that individual into providing sensitive information or money. These scams are common in phishing attempts and fraudulent schemes.

Infrastructure as a Service or IaaS

Infrastructure as a service or IaaS refers to a cloud computing model where providers offer virtualised computing resources via the internet. This allows businesses to access and manage servers, storage, and networking without the need for physical hardware. This is often preferred by scaling businesses as it is a more cost-effective solution for IT infrastructure.

Innovator

In fintech, an innovator is an individual or entity engaging with a financial technology service, utilising products such as banking, investment, or payment solutions. The term encompasses those who actively participate in and benefit from the offerings provided by fintech platforms, shaping the user base and driving the industry’s growth and innovation.

Instalments

The term instalments refers to the division of a payment into smaller, regular amounts over a defined and longer period. This can make it easier for consumers to afford purchases and also allows the seller to receive a steady guaranteed revenue.

Instrument

In the context of the financial industry, an instrument can be any tradable asset. This can include stocks, bonds, or derivatives, used for investment or hedging purposes.

InsurTech or Insurance Technology

InsurTech is short for Insurance Technology, this encompasses the use of technology and innovation to help improve and streamline the insurance industry and its services. This often involves the use of development of digital platforms as well as data analytics to enhance insurance processes.

Interchange

Interchange refers to the fees paid between banks for the processing of credit and debit card transactions. It plays a crucial role in the payment card industry’s functioning.

Interest Rate

An Interest Rate is the percentage at which interest is paid or charged on money that has a) been earned on invested funds or b) borrowed. The rate serves as an important tool for monetary policy as it influences borrowing and lending decisions, economic growth, and inflation. Central banks, such as the European Central Bank of the EU or the Bank of England in the UK, often use interest rates to manage the money supply and control economic conditions.

Investment

Investment is the act of providing money or resources with the expectation of creating income or profit in the future. As investment drives economic growth and wealth creation it is a fundamental concept in finance and economics.

Invoice Financing

Invoice finance, which is often also called accounts receivable financing or invoice factoring, is a method of finance whereby a business sells its unpaid invoices to a third party (factor) at a discount to access immediate funds. You can read about how Embedded finance for accounts payable works here.

Issuer

In the world of finance, an issuer is an entity that provides financial securities or instruments, e.g. stocks or bonds, for sale to investors. An issuer can be a government, corporation, or other organisation seeking capital.

K

Know your Business or KYB

Know your business or KYB is a due diligence process carried out to verify a corporate customer and its veracity and also assess the risk associated with such business customers. As a part of the KYB process, the legal entity’s representatives shall be identified while the Ultimate Beneficial Owners identified and verified. KYB helps prevent fraud and ensure regulatory compliance.

Know Your Customer (KYC)

Know Your Customer (KYC) is a due diligence process employed by financial institutions to verify the identity of individual customers (consumers) and assess the risk associated with their financial activities. KYC is fundamental for regulatory compliance and anti-money laundering.

L

Lender

A lender is an organisation, individual, or institution that makes funds available to borrowers with the expectation of the funds being repaid, typically with interest or fees incurred. Lenders could include credit unions, banks, online lending platforms, and other financial entities.

Liquidity

Liquidity describes how easily an investment, asset, or security can be sold or bought in the market – quickly and without significantly affecting its price. As the name implies, it’s a measure of how “liquid” an asset is. High-liquidity assets can be traded easily without a substantial impact on price, while low-liquidity assets can face price fluctuations during trading. Liquidity is paramount for the smooth functioning of financial markets, providing participants in the markets with the ability to enter and exit positions as they wish.

Liveness Check

A liveness check is a security measure used in identity verification processes, especially in digital or remote settings. The measure confirms that a person is physically present, i.e. they do not attempt to provide authentication by merely showing a static image or recording. Liveness checks typically use facial recognition or biometric data to confirm the live presence of a person.

Loan Disbursement

Loan disbursement releases approved funds to the borrower from the lender. Disbursement transfers the loan amount to the account of the borrower. Alternatively, in some cases, funds are disbursed directly to pay for expenses, e.g. tuition fees for educational loans.

Loan Orientation

Loan orientation is stage one of the lending process whereby a borrower applies for a loan and their application is evaluated by the lender. The borrower’s creditworthiness is used to decide whether a loan is approved or declined and involves collecting borrower information, credit checks, and documentation evidencing the borrower’s financial capability for loan repayments.

Loan Servicing

Loan servicing involves the ongoing management and administration of a loan after it has been orientated or disbursed. The process involves collecting payments, handling customer enquiries, managing escrow accounts for taxes and insurance and finally, ensuring compliance with the loan terms.

M

Merchant

A merchant is an individual or a business that sells goods or services to customers. Merchants are able to accept payments through multiple means, including cash, credit/debit cards, digital wallets and online payment gateways.

Micro-Enterprise

A micro-enterprise is defined as an enterprise which employs fewer than 10 persons and whose annual turnover and/or annual balance sheet total does not exceed EUR 2 million They usually operate at a local level such as self-employed individuals or family-owned individuals

MiFID

MiFID (Markets in Financial Instruments Directive 2014) is a f European Union directive that is used to govern financial markets and investment services. The aim is to increase transparency, investor protection and market integrity within the EU’s financial sector.

Mobile Wallet

A mobile wallet is a digital application or service allowing users to store, manage and make electronic transactions via their mobile devices. Mobile wallets can be used to store payment card information, loyalty cards and digital currencies to provide convenient and secure payments. We cover digital wallets and embedded finance in our article on “the benefits of Google Wallet and Apple Pay in the corporate world”

Modular Banking

Modular banking refers to the banking approach whereby financial institutions are able to build and customise their banking services using modular or interchangeable components. This enhances the flexibility and scalability of delivering banking services.

Money Laundering Reporting Officer or MLRO

A Money laundering reporting officer or MLRO is an individual designated within a financial institution who is responsible for overseeing and reporting suspicious transactions and/or activities that may involve financial crime or money laundering. They play an important role in the compliance of anti-money laundering (AML) regulations.

Multi-Currency Support

Multi-currency support is the financial system or service’s ability to process transactions and hold balances in multiple different currencies. This capability is crucial for businesses and individuals who engage in international trade or travel.

Multifactor Authentication

Multifactor authentication (MFA) is a type of security process that requires its users to provide two or more separate authentication factors in order to verify their identity. These factors usually include something a user knows (such as a password), something a user has (such as a mobile phone) and something a user is (such as facial recognition). This is a method of enhanced security and involves adding layers of verification.

N

Neobank

A neobank is a financial institution that operates mainly online and focuses on providing innovative and user-friendly banking services.

O

Offboarding

Offboarding is the process of managing an employee, customer, or user’s departure from an organisation or system. It includes tasks such as cancelling access to systems, doing exit interviews, and ensuring a smooth transition for the employee’s departure or removal from a system.

Office of Foreign Assets Control (OFAC)

The Office of Foreign Assets Control is an office in the U.S. Department of the Treasury responsible for enforcing economic and trading sanctions based on U.S. foreign policy and national security goals. OFAC keeps a list of individuals, entities, and countries with whom U.S. citizens and companies are restricted from engaging in certain transactions.

Offshore Banking Unit (OBU)

An Offshore Banking Unit or OBU is a branch/unit of a bank located in an overseas financial centre. . OBUs are mainly used for offshore financial services and provide benefits such as tax advantages and confidentiality.

Onboarding

Onboarding is the process of integrating a new employee, customer, or user into an organisation or system. It includes orientation, training, and familiarisation to ensure a smooth transition and effective integration.

Open API

Open API (Application Programming Interface) is a set of rules and protocols that makes it possible for different software applications to communicate with each other. Open APIs are available to developers and help the creation of third-party applications or services.

Open Banking

Open banking is the use of open Application Programming Interfaces (APIs) to enable third-party developers to build applications and services that can communicate with a bank’s customer data and systems. Read our article on the difference between Open Banking and Banking as a Service.

Open Banking Payments

Open banking payments are all the financial transactions done through open banking platforms and APIs. They give secure access to financial data and the ability to make payments directly from bank accounts.

Open Finance

Open finance is an extension of open banking that surrounds a bigger range of financial services and data-sharing more than just traditional banking.

Overdraft

The term overdraft refers to when a bank account holder withdraws or spends more money than is available in their account. This results in a negative balance, often the amount a person is able to withdraw is agreed upon with the bank, however, banks may charge fees or interest on overdrafts.

P

Primary Account Number or PAN

PAN or Primary Account Number refers to a unique alphanumeric code that is assigned to a payment card. These cards can include credit, debit cards or other cards that store values, the unique code identifies the issuing bank as well as the account holder. It is essential for the processing of card transactions.

Payee

The payee is the individual or entity with whom a payment is made. In a financial transaction, the payee receives the funds from the payer in exchange for goods, services or part of an agreement.

Payer

The payer is the party that is making a payment to the payee. This term is commonly used in financial contexts to identify the entity or individual who is responsible for disbursing funds.

Payment card industry (PCI)

Payment card industry (PCI) compliance refers to the adherence to security standards set by the Payment Card Industry Data Security Standard (PCI DSS). PCI is crucial for an organisation that handles payment card data in order to protect sensitive information and prevent data breaches.

Payment Execution

Payment execution is the process of initiating and completing a financial transaction from a payor to a payee. This can include transferring funds from one account to another. I

Payment Gateway

A payment gateway refers to the technology that allows businesses and individuals to accept electronic payments, this can include credit card transactions through their website or mobile applications.

Payment Initiation Service (PIS)

The term Payment Initiation Service (PIS) refers to a financial service that allows authorised third parties to initiate payments from a user’s bank account with their consent.

Payment Initiation Service Provider (PISP)

A Payment Initiation Service Provider (PISP) is a company or entity that offers Payment Initiation Services which enables a user to initiate payments from their bank accounts.

Payment Rails

Payment rails are the underlying infrastructure and networks which facilitate the movement of funds between financial institutions and accounts. Payment rails ensure the secure and efficient movement and transfer of money.

Payment Service Provider (PSP)

A Payment Service Provider (PSP) is an institution that offers payment processing services to merchants and businesses. PSPs enable companies to accept various forms of payment, such as credit cards and digital wallets.

Payment Service User (PSU)

A Payment Service User (PSU) is an individual or business entity that uses payment services to make or receive payments. PSUs can be customers or businesses.

Payment Services

Payment services include a broad range of financial services related to the transfer of money, including but not limited to payment processing, money transfers, and electronic payments.

PCI-DSS

PCI-DSS are security standards designed to protect payment card data and reduce the risk of data breaches. Compliance with PCI-DSS is mandatory for organisations that handle payment card information.

Peer-to-Peer (P2P)

Peer-to-peer (P2P) payments are electronic money transactions between people or entities using digital platforms or mobile applications. P2P payments enable users to send money directly to others without involving traditional financial institutions.

Personal Identification Number (PIN)

A personal identification number, or PIN, is a numeric code used for authentication and security purposes.

Platform Economy

The platform economy is an economic system where businesses use digital platforms to enable transactions between parties. These platforms connect service providers, consumers, and businesses in various industries, often in an online marketplace.

Plug-and-Play Finance

Plug-and-Play Finance refers to financial services or systems that are created for easy integration and use. This approach allows businesses to quickly adopt and utilise financial tools and services without comprehensive customisation or development. For information about how Weavr uses plug-and-play finance to embed finance into businesses check out our plug-and-play embedded finance solutions.

Point of Sale (PoS)

The Point of Sale is the location of the system for customers to pay for goods or services. This can include physical cash registers in brick-and-mortar stores or digital payment terminals for any online purchases.

Politically Exposed Person (PEP)

A Politically Exposed Person or PEP is an individual entrusted with a prominent public position, other than middle-ranking or more junior officials, or who has a close association with such a person. The list of prominent public functions at the national level, at the level of international organisations and at the level of EU institutions and bodies has been published in the EU Official Journal: EUR-Lex – 52023XC00724. PEPs are often exposed to enhanced scrutiny in financial transactions in order to prevent corruption, money laundering or other illicit activities.

Predicate Offence

A Predicate Offence is a criminal offence that is the basis of another offence. In money laundering cases, a predicate offence is the underlying criminal activity which generated the property laundered. An example of this is money laundering and the identification of predicate offences is crucial to law enforcement when investigating financial crimes.

Prepaid Card

A Prepaid Card is a payment card that has been preloaded with a specific amount of money. The balance can then be spent until it is exhausted, which is a more convenient and budget-friendly alternative to credit or debit cards.

Proceeds of Crime

Proceeds of Crime are any assets or funds that have been obtained through illegal activity. Law enforcement agencies work to confiscate and recover these proceeds to disrupt any criminal enterprises.

PSD2 (Second Payment Services Directive)

PSD2 is a European Union directive that is aimed at creating a more integrated payment service market within the European Union and enhancing the protection of customers. It promotes competition and innovation within the payment industry which also introduces strong customer authentication requirements.

Push-to-Card Payments

Push-to-card payments are when funds are sent directly to a payment card. These can include debit cards or prepaid cards and enable the fast and convenient distribution of funds to individuals.

R

Recurring Payment

A Recurring Payment is a regular financial transaction that occurs at specific, pre-decided intervals. It is often used for subscription services, utility bills and other ongoing expenses.

Regulatory Compliance

Regulatory Compliance refers to the adherence to laws, regulations and industry standards of an organisation relative to its operations.

Regulatory Sandbox

A Regulatory Sandbox is a controlled environment used for the purpose of testing innovative financial products and services. This is done under the supervision of regulatory authorities and allows for experimentation while maintaining consumer protection standards. Click here to try out Weavr’s embedded finance sandbox

Regulatory technology (Regtech)

Regulatory technology or Regtech is a type of technology solution designed to aid regulated businesses in complying with regulatory requirements more effectively. It provides software and tools for risk management, compliance monitoring and reporting.

Relative or Close Associate (RCA)

A Relative or Close Associate (RCA) is an individual who has a close relationship with an influential figure or a PEP. The individual may be subject to similar scrutiny in financial transactions as a result of their associations.

Remittance

Remittance involves cross-border money transfers from one party to another party. Usually, such payments are being made by foreign workers to their family members to support their financial needs.

Repayment

A Repayment is the return of any borrowed funds to a lender or creditor. This includes the principal amount and any interest or fees, as applicable.

Retail Banking

Retail Banking refers to the division of banking serving small businesses or individual consumers. These services include savings accounts, loans, mortgages and basic financial products.

Revenue Finance

Revenue Finance involves securing funding by offering investors a share of the company’s future revenue in exchange for capital, without traditional debt or equity.

Revenue Sharing

Revenue sharing is a financial agreement where parties involved agree to share a portion of the revenue that is generated from a specific business activity or venture.

Risk Assessment

A Risk Assessment is the process of evaluating the potential risks and vulnerabilities associated with an organisation or system. It helps to identify, analyse and mitigate risks and ensure business continuity.

Risk Management

Risk Management involves the strategies and practices used to identify, access and control risks with the aim of minimising potential negative impacts on an organisation’s objectives.

Risk-Based Approach (RBA)

A Risk-Based Approach or RBA is a method used to manage risk and prioritise resources and actions based on the level of risk involved. This approach is commonly used in regulatory compliance and financial services.

Return on Investment (ROI)

Return on investment or ROI is a financial metric that is used to evaluate an investment’s profitability. The metric is used to measure the gain or loss relative to the cost of the original investment.

S

Safeguarding

Safeguarding is a requirement for Payment Institutions and Electronic Money Institutions to protect customers’ funds and ensure that in case of insolvency, such institutions will be able to return the funds to their customers.

Sanctions

Sanctions are any restrictions or penalties imposed by governments or international bodies on entities, countries, regions or individuals in order to achieve foreign policy or security objectives. Sanctions can include travel bans, asset freezes, arms embargoes, and trade restrictions.

Sandbox

A Sandbox is a controlled and isolated environment that allows software and applications to be tested and developed without having an effect on the production environment itself. Click here to explore Weavr’s embedded finance sandbox.

Savings

Savings refers to any money unspent but instead set aside for future use in emergencies and is a fundamental part of financial planning.

SCT-Inst (SEPA Instant)

SCT-Inst (SEPA Instant) is a payment scheme that exists within the Single Euro Payments Area (SEPA). It enables instant credit transfers between participating banks in Europe.

Service organisation controls (SOC)

Service organisation controls or SOC reports are independent assessments of a service organisation’s controls related to security, availability, processing integrity, confidentiality and privacy. These assessments provide assurance to the customers and stakeholders of the organisation.

Single Sign-On (SSO)

Single Sign-On or SSO is an authentication process that permits users to access multiple applications or systems using one set of login credentials.

SME (Small to medium-sized business)

SME is the term used to describe businesses smaller in scale than larger corporations and whose staff numbers and economic weight fall below certain limits.

- A medium-sized company has up to 250 employees, a turnover of up to €50 million and a balance sheet total of up to €43 million;

- A small company has up to 50 employees and a turnover or balance sheet total of up to €10 million;

- A micro-company has up to 10 employees and a turnover or balance sheet total of up to €2 million.

These smaller businesses play a significant role in economic and employment growth.

Software as a Service (SaaS)

Software as a Service or SaaS refers to a cloud computing model where software applications can be hosted and accessed on a subscription basis over the internet.

Source of Funds

The source of funds is the origin or provenance of the money used in financial transactions. It is essential that funds are verified to confirm they come from legitimate sources.

Source of Wealth

Source of Wealth refers to the means by which an entity or an individual has accumulated their assets and financial resources. This is assessed to ensure they comply with anti-money laundering (AML) regulations.

Special Interest Entity (SIE)

A Special Interest Entity or SIE is an entity or organisation with specific interests or objectives, that is often related to lobbying, advocacy or special causes.

Special Interest Person (SIP)

A Special Interest Person or SIP is an individual who is associated with or actively involved with special entities or causes.

Spend Controls

Spend controls are set by organisations to manage and control expenditures effectively in accordance with their policies and limits. Discover how Embedded Finance gives you full control of user spending in our ultimate guide to embedded finance.

Spend Limit

A Spend Limit is a maximum sum of money that can be charged or spent within a specific period of time, usually set by a financial institution or card issuer.

Split Payments

Split Payments is a method of transaction where payment is divided into multiple parts and is transferred to different recipients or accounts.

Standing Order

A standing order is a payment instruction that has been pre-authorised and directs a bank to make regular payments, often on a fixed schedule, to a particular person or organisation.

Statement

A statement is a financial document that contains a summary of transactions, account balances and other relevant information related to a financial account over a specific period, usually issued monthly.

Strong Customer Authentication (SCA)

Strong customer authentication or SCA requires customers to provide multiple forms of authentication and is used as a security measure to access sensitive online services. Read our article on strong customer authentication in embedded finance

Suspicious Activity Report (SAR) / Suspicious Transaction Report (STR)

SARs and STRs are reports submitted to authorities by financial institutions in case of any suspicion or having reasonable grounds to suspect that a customer’s transaction or activity may involve illegal activities or financial crime, including but not limited to money laundering.

Sustainable Finance

Sustainable Finance considers the social, environmental, and governance (ESG) factors of financial practices and investments while also promoting long-term sustainability.

T

Third-Party Provider (TPP)

A Third-Party Provider or TPP is an external entity that offers access to financial data or financial services on behalf of a customer, usually with consent from the customer.

Time to Market (TTM)

Time to market describes the time it takes to develop, produce and establish a product or service to the market and is a huge factor in competitiveness.

Tipping Off

Tipping off is a criminal offence as it’s the act of disclosing to an individual that they are the subject of a suspicious activity report or investigation, potentially hindering law enforcement efforts.

Tokenisation

Tokenisation involves replacing sensitive data with a unique identifier (also known as a token) to enhance the security of sensitive information and to help protect it.

Total Cost of Ownership (TCO)

Total cost of ownership or TCO is a financial estimate used to calculate the total costs of owning, operating and maintaining an asset or product over its entire lifecycle.

Transaction

A transaction involves the exchange of goods, services or financial assets between one or more parties. it can include various types of activities, including purchases, sales and transfers.

Transaction Confirmation Service (TCS)

Transactional confirmation service or TCS confirms successful financial transactions, in real-time, to enhance transparency and security.

Transaction Monitoring

Transaction monitoring involves consistently reviewing financial transactions to identify and report any suspicious or unusual activity. This factors in anti-money laundering (AML) efforts.

U

Ultimate Beneficial Owner (UBO)

An Ultimate Beneficial Owner is a natural person who ultimately owns or controls a legal entity or body of persons through the direct or indirect ownership of a sufficient percentage (usually more than 25%) of shares, voting rights or ownership interest. In some circumstances, the UBO shall be identified as a person exercising control over the entity via other means. If no beneficial owner is identified in accordance with the above, the natural person(s) who hold(s) the position of senior managing official or officials need to be identified.

United Kingdom Financial Intelligence Unit (UKFIU)

The United Kingdom Financial Intelligence Unit or UKFIU is a government agency responsible for receiving, analysing and disseminating financial intelligence in regards to money laundering and terrorist financing within the United Kingdom.

Unsecured Lending

Unsecured lending relates to providing loans to borrowers without requiring collateral. A borrower’s creditworthiness is used by the lender to assess the risk.

User experience (UX)

User experience or UX includes the overall interaction and satisfaction of users when interacting with services, products or digital interfaces.

User Interface (UI)

User interface or UI refers to the layout and design of a digital platform, application or device that users interact with.

V

Variable Recurring Payment

A variable recurring payment is a repeated transaction with a changing or variable amount. This is often used for bills or subscriptions with fluctuating costs.

Vertically Integrated

Vertically integrated refers to a business model where a company controls more than one stage of the production or supply chain, from raw materials to distribution.

Virtual Card

A virtual card is a digital payment card that solely exists in electronic form and is used for online or remote transactions. Read our article outlining how Weavr uses virtual cards for employee benefits providers.

Vulnerable Customer

A vulnerable customer is an individual who has the potential to be at risk of financial harm as a result of specific circumstances or characteristics. This may result in this individual requiring special consideration and protection.

W

Webhook

A Webhook allows one application to send real-time data to another application or system in order to trigger events are actions

White-Label Banking

White-label banking is where a financial institution provides its products or services under another company’s brand. This allows businesses to offer banking services without developing them from scratch.

Wire Transfer

Outgoing wire transfer is a process of transferring funds from one bank account to another electronically. It’s commonly used for domestic and international money transfers and it is fast and very secure.